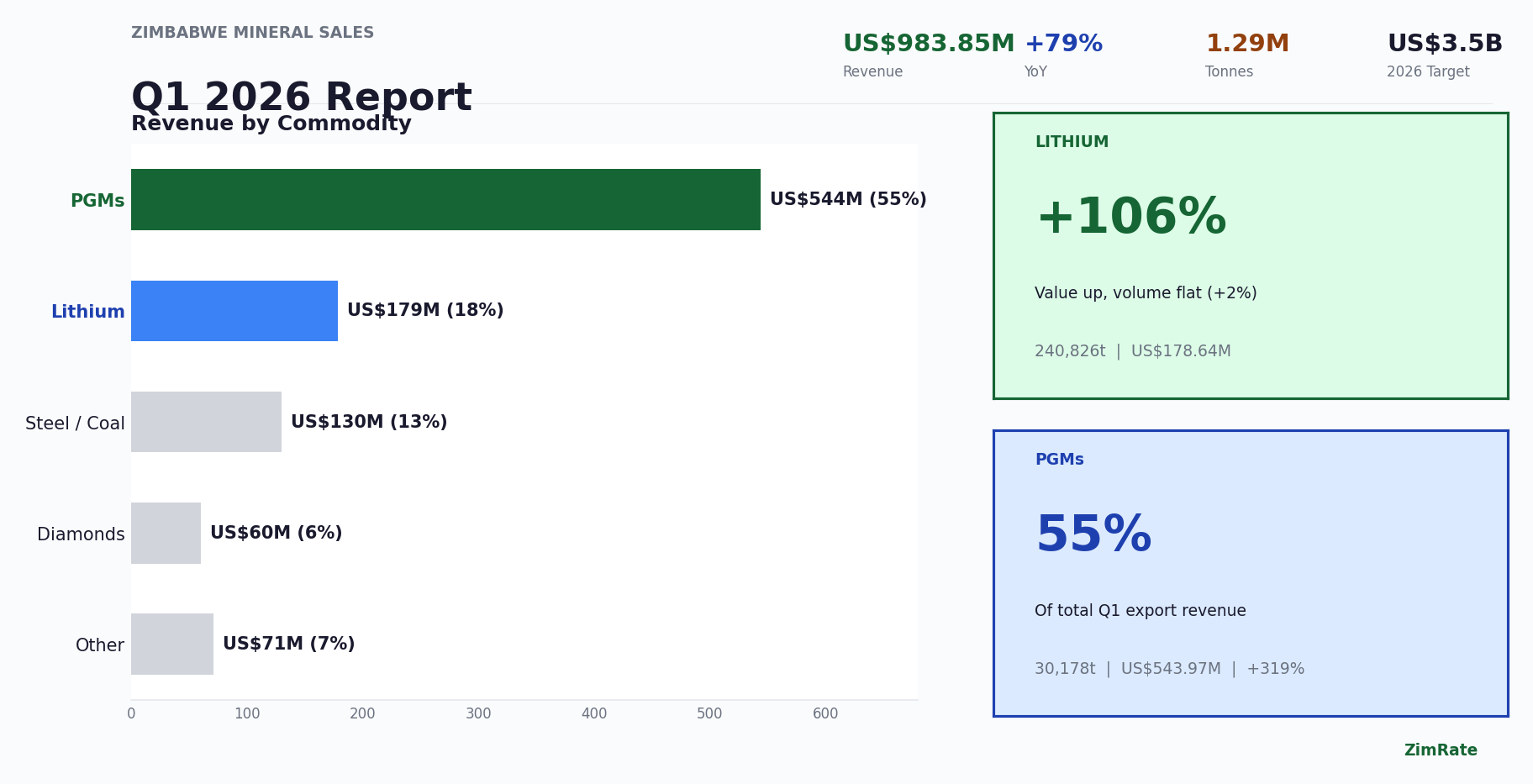

Zimbabwe's mining sector posted its strongest quarterly performance on record in the first three months of 2026, with mineral sales reaching US$983.85 million. The figure represents a 79% jump in revenue compared to the same period last year, driven largely by the government's controversial ban on raw mineral exports.

The Minerals Marketing Corporation of Zimbabwe (MMCZ), which manages the country's mineral exports, reported total sales of 1,288,761 metric tonnes across all commodities. Volume was up 27% year-on-year, but the real story is in the value. Beneficiation, the process of adding value to raw minerals before export, is beginning to reshape how Zimbabwe participates in global mineral markets.

PGMs Lead the Charge

Platinum Group Metals generated US$543.97 million in export revenue, making them the single largest contributor. PGM concentrate sales surged to 30,178 metric tonnes worth US$191.73 million, a 319% increase in value despite a 98% rise in volume (Zimbabwe Now). The numbers point to higher prices per unit, a direct result of Zimbabwe pushing miners to process more platinum locally before shipping it overseas.

Zimplats, the country's biggest platinum producer, has invested US$190 million in refinery rehabilitation to meet the new beneficiation requirements (Equity Axis). The company's smelter operations now produce PGM matte, a processed form that commands significantly higher prices than raw concentrate.

Lithium: Flat Volume, Surging Value

Lithium tells the most striking story. Sales reached 240,826 metric tonnes valued at US$178.64 million, a 106% increase in value. But volumes grew by just 2% (Zimbabwe Now). That gap between value and volume is the entire point of the export ban.

Before February, Zimbabwe shipped raw spodumene concentrate to China, where it was processed into battery-grade lithium chemicals. The country earned roughly US$375 per tonne for material that, once processed overseas, sold for up to US$20,000 per tonne (Prospect Intel). Zimbabwe was bearing the extraction costs while Chinese firms captured the margins.

The ban, imposed on 25 February 2026, stopped that overnight. It applied to all raw minerals and lithium concentrates, including shipments already in transit. The government had originally planned to phase out lithium concentrate exports from 2027, but accelerated the timeline after detecting what it called "widespread malpractices and leakages" in the export chain (Reuters).

China Feels the Pressure

Zimbabwe supplies approximately 15% of the spodumene imported into China, making it a critical link in the global battery supply chain (Fastmarkets). Chinese mining firms, including Zhejiang Huayou Cobalt, Sinomine Resource Group, Chengxin Lithium, and Yahua Industrial Group, have invested more than US$1.4 billion in Zimbabwe's lithium operations (African Insider).

The ban forced those companies to rethink their strategy. Huayou's subsidiary, Prospect Lithium Zimbabwe, completed a US$400 million processing plant at Arcadia and shipped Africa's first lithium sulphate consignment in April 2026. The facility has nameplate capacity of 50,000 tonnes annually, but that processes just 4% of Zimbabwe's 2025 concentrate exports (Prospect Intel).

Sinomine has announced a US$500 million sulphate plant at Bikita, Zimbabwe's largest lithium mine, but that project is still in planning stages.

The Cost of Speed

The numbers are impressive, but the ban has not been painless. MMCZ disclosed it is absorbing roughly US$462,000 per month in lost commission revenue from the lithium restriction alone (Zimbabwe Independent). Industry sources estimate the broader impact at around US$60 million monthly in royalties and taxes no longer flowing to Treasury.

Five major lithium producers, employing about 9,000 workers, have scaled down operations and are stockpiling ore while they wait for processing capacity to catch up. Some smaller operators have mothballed entirely (Zimbabwe Independent).

Diamond exports also remained under pressure, weighed down by falling prices and growing competition from lab-grown stones (Africa Business Insider).

What Comes Next

MMCZ has set a US$3.5 billion revenue target for 2026. The Q1 run rate of nearly US$1 billion suggests the target is within reach, provided PGM and lithium prices hold steady and beneficiation capacity continues to expand.

The government is now reviewing its lithium export quota system, which replaced the outright ban in April. Companies with approved processing plans can apply for export permits, but a full concentrate ban takes effect in January 2027 (MiningFocus Africa).

For Zimbabwe, the stakes are clear. The country sits on some of Africa's largest lithium reserves and ranks among the world's top PGM producers. Whether it can capture more of the value chain will depend on energy supply, infrastructure investment, and the speed at which miners build local processing capacity.

Readers can track exchange rates and commodity pricing on the ZimRate USD/ZiG converter, and follow our coverage of Zimbabwe fuel pricing trends.

This article is for informational purposes only and does not constitute financial advice.